Know the Tax Incentives Available to you*. The IRS requires that equipment be in use (not just purchased) by December 31 to qualify for these deductions. We have inventory on the lot making it possible for you to meet this qualification. Call us at (757) 465-2200 to buy today.

- Immediate Deduction Under Section 179

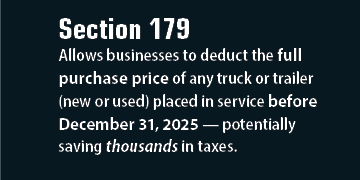

The Section 179 deduction allows businesses to deduct the full purchase price of qualifying equipment (new or used) that is placed in service before year-end, rather than depreciating it over several years.

- 2025 deduction limit (indexed annually): around $1.22 million.

- Phase-out threshold: begins when total equipment purchases exceed $3.05 million.

- Applies to: trucks, trailers, machinery, computers, office furniture, and other tangible business assets.

Example: If you buy $100,000 of equipment and put it into service before Dec 31, you can deduct the full $100,000 this year—potentially saving $20–30K in taxes depending on your bracket.

- Bonus Depreciation (100% / 60%)

In addition to or instead of Section 179, businesses can use bonus depreciation on new or used equipment.

- Under current law, bonus depreciation is 60% for 2025 (phasing down from 80% in 2023 and 100% in prior years).

- It’s applied automatically to eligible property unless you opt out.

- Unlike Section 179, bonus depreciation can create a net loss, which can offset other taxable income.

Example: If you purchase $500,000 in equipment and elect 60% bonus depreciation, you can deduct $300,000 immediately and depreciate the rest over its normal life.

- Reducing Estimated Tax Payments and Boosting Cash Flow

By accelerating deductions into the current year, you can:

- Reduce taxable income for 2025.

- Lower quarterly estimated tax payments.

- Improve year-end cash flow, since you keep more money in the business rather than paying it out in taxes.

- Locking in Incentives Before Law Changes

Tax rules change frequently—especially around depreciation limits and bonus percentages. Purchasing and placing equipment into service by December 31 locks in:

- The current year’s Section 179 and bonus depreciation rates, and

- The value of deductions before further phase-outs occur in later years.

- What “Placed in Service” Means

The IRS requires that equipment be in use (not just purchased) by December 31 to qualify for these deductions.

- Merely signing a purchase order or paying for the equipment isn’t enough—it must be installed, operational, and ready for business use.

*Disclaimer: This information is for general reference only and is not tax advice. Consult your qualified tax professional for details.

Available Inventory

| Stock Number: | ROR-20Y-2242-SC |

| Type: | Roll Off Container |

| Exterior Color: | Black |

| Stock Number: | 14912N |

| Type: | Rollbacks |

| Manufacturer: | Peterbilt |

| Model: | 536 |

| Exterior Color: | Red |

| Engine Manufacturer: | Paccar |

| Engine Type: | PX-7 |

| Transmission: | Allison 2500RDS |

| Stock Number: | 14871U |

| Type: | Wreckers |

| Mileage: | 136,008 |

| Manufacturer: | International |

| Model: | CV |

| Exterior Color: | Red |

| Engine Type: | 6.6L |

| Stock Number: | 14847N |

| Type: | Landscape Dump |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | Black |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2500RDS |

| Stock Number: | 14910N |

| Type: | Box Truck |

| Manufacturer: | Isuzu |

| Model: | NRR |

| Exterior Color: | White |

| Transmission: | Allison 1000 RDS |

| Stock Number: | 14909N |

| Type: | Box Truck |

| Manufacturer: | Isuzu |

| Model: | NRR |

| Exterior Color: | White |

| Transmission: | Allison 1000 RDS |

| Stock Number: | 14587N |

| Type: | Box Truck |

| Manufacturer: | Isuzu |

| Model: | FTR |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | B6.7 L |

| Transmission: | Allison 2550 RDS |

| Stock Number: | 14844N |

| Type: | Wreckers |

| Manufacturer: | Peterbilt |

| Model: | 567 |

| Exterior Color: | Red |

| Engine Manufacturer: | Cummins |

| Engine Type: | ISX 15 |

| Transmission: | Eaton Fuller |

| Stock Number: | ROR-20Y-2242-SC |

| Type: | Roll Off Container |

| Exterior Color: | Black |

| Stock Number: | 14585N |

| Type: | Landscaper |

| Manufacturer: | Isuzu |

| Model: | NPR |

| Exterior Color: | White |

| Engine Type: | 6.6L |

| Transmission: | Hydro-Matic |

| Stock Number: | 14836U |

| Type: | Box Truck |

| Mileage: | 164,605 |

| Manufacturer: | Isuzu |

| Model: | NPR |

| Exterior Color: | White |

| Engine Manufacturer: | GMPT |

| Engine Type: | 6.6L |

| Stock Number: | 14775N |

| Type: | Wreckers |

| Manufacturer: | Kenworth |

| Model: | T880 |

| Exterior Color: | Black |

| Engine Manufacturer: | Cummins |

| Engine Type: | X-15 |

| Transmission: | Allison 4700RDS |

| Stock Number: | 14427N |

| Type: | Roll Off |

| Manufacturer: | Western Star |

| Model: | 49X |

| Exterior Color: | White |

| Engine Manufacturer: | Detroit |

| Engine Type: | DD13 |

| Transmission: | Detroit DT12 |

| Stock Number: | 14709U |

| Type: | Roll Off |

| Mileage: | 107,664 |

| Manufacturer: | Kenworth |

| Model: | T370 |

| Exterior Color: | White |

| Engine Manufacturer: | Paccar |

| Engine Type: | PX-9 |

| Transmission: | Allison 3000RDS |

| Stock Number: | 14744U |

| Type: | Platform/Stake Body |

| Mileage: | 90127 |

| Manufacturer: | Freightliner |

| Model: | 114SD |

| Exterior Color: | White |

| Engine Manufacturer: | Detroit |

| Engine Type: | DD13 |

| Transmission: | Allison 4500RDS |

| Stock Number: | 14496N |

| Type: | Rollbacks |

| Manufacturer: | International |

| Model: | MV |

| Exterior Color: | Black |

| Engine Manufacturer: | Cummins |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14745N |

| Type: | Roll Off |

| Manufacturer: | International |

| Model: | MV |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | B6.7 L |

| Transmission: | Allison 3500RDS |

| Stock Number: | 14782N |

| Type: | Trailers |

| Manufacturer: | Cottrell |

| Trailer Model: | CX-5308LS |

| Stock Number: | 14934N |

| Type: | Landscape Dump |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | Black |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14940N |

| Type: | Box Truck |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | B6.7 L |

| Transmission: | Allison 2500RDS |

| Stock Number: | 14939N |

| Type: | Box Truck |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | B6.7 L |

| Transmission: | Allison 2500RDS |

| Stock Number: | 14908N |

| Type: | Platform/Stake Body |

| Manufacturer: | Ford |

| Model: | F-550 |

| Exterior Color: | White |

| Engine Manufacturer: | Ford |

| Engine Type: | 7.3L V8 |

| Transmission: | TorqShift |

| Stock Number: | 14987N |

| Type: | Mason Dump |

| Manufacturer: | Ford |

| Model: | F-550 |

| Exterior Color: | White |

| Engine Manufacturer: | Ford |

| Engine Type: | 7.3L V8 |

| Transmission: | TorqShift Automatic |

| Stock Number: | 14986N |

| Type: | Mason Dump |

| Manufacturer: | Ford |

| Model: | F-550 |

| Exterior Color: | White |

| Engine Manufacturer: | Ford |

| Engine Type: | 7.3L V8 |

| Transmission: | TorqShift Automatic |

| Stock Number: | 14985N |

| Type: | Mason Dump |

| Manufacturer: | Ford |

| Model: | F-550 |

| Exterior Color: | White |

| Engine Manufacturer: | Ford |

| Engine Type: | 7.3L V8 |

| Transmission: | TorqShift Automatic |

| Stock Number: | 14937N |

| Type: | Landscape Dump |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | Black |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2500RDS |

| Stock Number: | 14590N |

| Type: | Box Truck |

| Manufacturer: | Isuzu |

| Model: | NPR |

| Exterior Color: | White |

| Engine Manufacturer: | GMPT |

| Engine Type: | 6.6L |

| Transmission: | Hydro-Matic |

| Stock Number: | 14781N |

| Type: | Trailers |

| Manufacturer: | Cottrell |

| Trailer Model: | CX-5308LS |

| Stock Number: | 14929N |

| Type: | Chipper Body |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14930N |

| Type: | Chipper Body |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14928N |

| Type: | Chipper Body |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14931N |

| Type: | Chipper Body |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14967N |

| Type: | Rollbacks |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14968N |

| Type: | Rollbacks |

| Manufacturer: | Hino |

| Model: | L6 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14949N |

| Type: | Wreckers |

| Manufacturer: | Dodge |

| Model: | 4500 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L Turbo Diesel |

| Transmission: | TorqueFlite |

| Stock Number: | 14383U |

| Type: | Car Haulers |

| Mileage: | 749052 |

| Manufacturer: | Peterbilt |

| Model: | 388 |

| Exterior Color: | Mocha / Blue |

| Engine Manufacturer: | Cummins |

| Engine Type: | X-15 |

| Transmission: | Eaton Fuller |

| Trailer Model: | CX-10HCS |

| Stock Number: | 14503N |

| Type: | Rollbacks |

| Manufacturer: | International |

| Model: | MV |

| Exterior Color: | Red |

| Engine Manufacturer: | Cummins |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14667U |

| Type: | Rollbacks |

| Stock Number: | 14495U |

| Type: | Trailers |

| Exterior Color: | White |

| Stock Number: | 13442N |

| Type: | Wreckers |

| Manufacturer: | Western Star |

| Model: | 49X |

| Exterior Color: | White |

| Engine Manufacturer: | Detroit |

| Engine Type: | DD16 |

| Transmission: | Allison 4700RDS |

| Stock Number: | 14408U |

| Type: | Wreckers |

| Manufacturer: | Peterbilt |

| Model: | 567 |

| Exterior Color: | Red |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Stock Number: | 13982N |

| Type: | Rollbacks |

| Manufacturer: | Peterbilt |

| Model: | 536 |

| Exterior Color: | Black |

| Engine Manufacturer: | Paccar |

| Engine Type: | PX-7 |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14251N |

| Type: | Knuckle Boom Crane |

| Manufacturer: | Freightliner |

| Model: | M2 |

| Exterior Color: | White |

| Engine Manufacturer: | Detroit |

| Engine Type: | DD8 |

| Transmission: | Allison 3000RDS |

| Stock Number: | 14499N |

| Type: | Rollbacks |

| Manufacturer: | International |

| Model: | MV |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Transmission: | Allison 2200 RDS |

| Stock Number: | 14263N |

| Type: | Wreckers |

| Manufacturer: | Kenworth |

| Model: | T880 |

| Exterior Color: | Viper Red |

| Engine Manufacturer: | Cummins |

| Engine Type: | X-15 |

| Transmission: | Eaton Fuller |

| Stock Number: | 13894N |

| Type: | Rollbacks |

| Manufacturer: | Isuzu |

| Model: | FTR |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | 6.7L |

| Transmission: | Allison 2550 RDS |

| Stock Number: | 14350N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | White |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Paccar TX-12 |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 13543N |

| Type: | Roll Off |

| Manufacturer: | Isuzu |

| Model: | NRR |

| Exterior Color: | White |

| Engine Type: | 6.6L |

| Transmission: | Allison 1000 RDS |

| Stock Number: | ROR-S30SC2260 |

| Type: | Roll Off Container |

| Exterior Color: | Black |

| Stock Number: | 14090N |

| Type: | Wreckers |

| Manufacturer: | Ford |

| Model: | F-450 |

| Exterior Color: | Black |

| Engine Manufacturer: | Ford |

| Engine Type: | 6.7L Powerstroke V8 |

| Transmission: | Automatic |

| Stock Number: | 13853N |

| Type: | Wreckers |

| Manufacturer: | Kenworth |

| Model: | T880 |

| Exterior Color: | White |

| Engine Manufacturer: | Cummins |

| Engine Type: | X-15 |

| Transmission: | Allison 4700RDS |

| Stock Number: | 13496N |

| Type: | Roll Off |

| Manufacturer: | Western Star |

| Model: | 49X |

| Exterior Color: | White |

| Engine Manufacturer: | Detroit |

| Engine Type: | DD13 |

| Transmission: | Allison 4500RDS |

| Stock Number: | 14789N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | White |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Paccar TX-12 |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 14780N |

| Type: | Trailers |

| Manufacturer: | Cottrell |

| Trailer Model: | C-5305LS |

| Stock Number: | 14779N |

| Type: | Trailers |

| Manufacturer: | Cottrell |

| Trailer Model: | C-5305LS |

| Stock Number: | 14777N |

| Type: | Trailers |

| Manufacturer: | Cottrell |

| Trailer Model: | C-5305LS |

| Stock Number: | 14776N |

| Type: | Trailers |

| Manufacturer: | Cottrell |

| Trailer Model: | C-5305LS |

| Stock Number: | 14791N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | White |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Eaton Endurant |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 14793N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | White |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Eaton Endurant |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 14797N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | Quicksilver Effect |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Paccar TX-12 |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 14801N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | Quicksilver Effect |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Paccar TX-12 |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 11505U |

| Type: | Trailers |

| Manufacturer: | Dorsey |

| Exterior Color: | White |

| Stock Number: | 14799N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | White |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Paccar TX-12 |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 14795N |

| Type: | Car Haulers |

| Manufacturer: | Peterbilt |

| Model: | 589 |

| Exterior Color: | Viper Red |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Paccar TX-12 |

| Trailer Model: | CX-09LSFA |

| Stock Number: | 14073N |

| Type: | Roll Off |

| Manufacturer: | Freightliner |

| Model: | M2 106 |

| Exterior Color: | White |

| Engine Manufacturer: | Detroit |

| Engine Type: | DD8 |

| Transmission: | Allison 3500RDS |

| Stock Number: | 14591N |

| Type: | Landscaper |

| Manufacturer: | Isuzu |

| Model: | NPR |

| Exterior Color: | White |

| Engine Type: | 6.6L |

| Transmission: | Hydro-Matic |

| Stock Number: | ROR-20Y-2242-SC |

| Type: | Roll Off Container |

| Exterior Color: | Black |

| Stock Number: | 14616U |

| Type: | Car Haulers |

| Mileage: | 681,199 |

| Manufacturer: | Peterbilt |

| Model: | 389 |

| Exterior Color: | Orange |

| Engine Manufacturer: | Paccar |

| Engine Type: | MX-13 |

| Transmission: | Eaton Fuller |

| Trailer Model: | CX-09LS3 |

| Stock Number: | 14671U |

| Type: | Rollbacks |

| Mileage: | 86,485 |

| Manufacturer: | Freightliner |

| Model: | M2 |

| Exterior Color: | Black |

| Engine Manufacturer: | Detroit |

| Engine Type: | DD8 |

| Transmission: | Allison 3000RDS |